An Interview with Allison B. Becker, CRPC®, APMA®

The Community Foundation recently sat down with Allison B. Becker, a Financial Advisor, Fiduciam Financial of the private wealth advisory practice of Ameriprise Financial Services, LLC to discuss charitable giving as part of comprehensive financial planning.

An Interview with Allison B. Becker, CRPC®, APMA®

The Community Foundation recently sat down with Allison B. Becker, a Financial Advisor, Fiduciam Financial of the private wealth advisory practice of Ameriprise Financial Services, LLC to discuss charitable giving as part of comprehensive financial planning.

NCCF: Tell us a about your practice.

AB: We’re an independent financial firm backed by Ameriprise Financial. We work with clients in almost all 50 states. We hold ourselves to the highest standard in providing our clients with the highest level of service and as Fiduciaries, we put our clients‘ best interest before our own. We work to inspire confidence, simplify life, and reduce stress in our clients’ lives. In Connecticut, we have offices in Litchfield and New Haven County.

NCCF: How do you work with your clients to achieve their financial goals?

AB: I work with clients in a more collaborative approach. It’s important not only to provide my clients with recommendations, but to allow them to be part of the process as well. This is their financial journey. I like my clients to think about their financial future as a road. We want to avoid all potholes, ensure that the road is paved from point A to point B, and that the ride is as smooth as possible. It’s not only their investments that need to be included in their financial journey, but many other large decisions in life. I work with clients to uncover what’s important to them and the “why” behind their goals.

NCCF: You mentioned that you focus on clients’ entire financial journey. How does charitable giving fit into that journey?

AB: Our firm is very connected to the community. Twice a year we close our office for a national day of service. On that day, we volunteer at local nonprofits. Many of my clients who are very generous are also very connected to their communities. I enjoy helping them work toward and achieve their charitable goals in the most efficient and appropriate manner. Estate and Legacy planning are an important part of our financial coaching process. It’s helpful to have clients uncover their estate and legacy planning goals and to help create an action plan.

Giving charitably often becomes a great interest when clients must take distributions. They often do not need the money, and they see it as an opportunity to give back in their community. The effects of the pandemic have really increased charitable conversations. We all see the effects of the pandemic and its economic aftermath in our communities. Many of my clients want to leave a legacy, but given the current events, they also want to help now. It feels good to give back—knowing that you have done something for someone else. Keeping that giving local is an added benefit.

I was born and raised in Northwest CT. I believe, and many of my clients believe, that charitable giving can make a positive difference right here in the northwest corner. Giving locally provides transparency. My clients can see the improvements from their giving in their communities. It’s beneficial for the donors and nonprofits.

NCCF: What are some of the more popular planning mechanisms for giving?

AB: Many clients look to complete a qualified charitable donation using their required minimum distributions from their IRA assets. Other clients have highly appreciated stock holdings that they’re looking to use to help fund their charitable desires. We work together to decide how much should be given for charitable purposes based on the tax benefit and other legacy planning and/or charitable giving options to discuss and decide from.

When a client doesn’t know exactly what charity they want to donate to, but they want to stay local, we think about utilizing a donor-advised fund. I’ve helped clients create charitable funds through the Northwest CT Community Foundation, including scholarships, charitable remainder trusts, and charitable lead trusts. With the most recent SECURE ACT changes (increasing RMD/changes to inherited IRAs) and other tax laws up for discussion, planning is an on-going process. It’s important that people work with someone who can coach them through all of their life changes and ensure they have all their options in front of them to help them make the best decisions.

GOLDEN AGE FOR GIFT ANNUITIES

The American Council on Gift Annuities reports that the most popular age for funding an initial gift annuity is mid-70's. Because the Quiet Generation was born during the Great Depression and World War II, the number of babies was lower during both times of great distress. The Quiet Generation reached age 75 starting in 2005. Because of low birth rates for the Quiet Generation, the number of Americans turning age 75 each year has been lower than previous generations for the past decade.

However, in 1946 the fifteen million Americans who served in the military during World War II returned home and started families. As a result, the Baby Boomer generation (born 1946 to 1964) has nearly double the number of individuals turning age 75 each year when compared with the Quiet Generation. Because the senior Baby Boomers are now age 76, during the next two decades there will be steady growth in the size of the primary gift annuity market. With greatly increased numbers of potential gift annuitants, the coming decade is likely to be a golden age for gift annuities.

Many donors fund a gift annuity with cash. However, with the growth of stock values the past decade, donors with appreciated stock may use that asset to fund an immediate gift annuity.

Current or Immediate Gift Annuities

A gift annuity is a contract between the charity and the donor. The donor transfers property to the charity and the charity promises to pay the annuity for one life or two lives. Sec. 514(c)(5). Donors may choose between immediate payments to the annuitant or deferred payment schedules to the annuitant. Immediate gift annuities start making payments typically within on payment period from the funding date. Deferred gift annuities must delay payments at least one year from the funding date.

As a contractual obligation, the annuity payments are secured by the assets of the charity. Most charities maintain an annuity reserve fund, which is required by some state insurance commissioners. However, the endowment and all of the real property and other assets of the charity stand behind the promise to pay a gift annuity. Most nonprofits who issue gift annuities have large reserves that assure gift annuitants the full payments will be made.

Payout Taxation – Appreciated Property Annuity

If a donor funds a gift annuity with appreciated property, the taxation of payouts will need to take into consideration the long-term capital gain. If the annuity is nonassignable, except to the issuing charity, and the annuity is written for the life of the donor or life of donor and spouse, the capital gain in the annuity portion may be prorated. Reg. 1.1011-2(a)(4). In the case of a gift annuity funded with appreciated property, the capital gain on the gift portion is bypassed, while the capital gain prorated to the annuity portion will then be recognized over the life expectancy of donor or lives of donor and spouse.

If the donor is not the annuitant, the capital gain allocated to the gift portion is still bypassed. However, when the donor is not the annuitant and a child, nephew, niece or friend is the annuitant, the capital gain on the annuity contract portion will be recognized and reported by the donor in the year of the gift.

Mary Funds a Gift Annuity with Stock

Mary Johnson (age 80) owns stock purchased seven years ago for $2,000, with a current fair market value of $10,000. She transfers that stock in exchange for a charitable gift annuity. Her charitable deduction is $4,908 and the annuity contract value is $5,092. The portion of the $8,000 capital gain allocated to the charitable gift is bypassed. However, the capital gain allocated to the annuity contract must be reported during her life expectancy.

Based upon the life expectancy and the exclusion ratio, she reports ordinary income of $138.04 annually. However, the remaining amount that is excluded from ordinary income is now divided between the long-term capital gain and the tax-free return of basis. Prorating the capital gain over her years of expectancy, the capital gain each year is $433.35 and the tax-free amount is $108.61.

A few very senior persons may have a short life expectancy. For these gift annuity donors, the prorated capital gain may not exceed the excluded amount. That is, all of the excluded amount may be capital gain. The tax-free return may be reduced to zero, but not below zero.

It is possible for a gift annuity to be funded with long-term capital gain property and for the deduction to be based on the property's cost basis rather than fair market value. This option is helpful for a donor who desires to make a large gift of appreciated stock and has a reasonably high basis. The donor must elect to base the deduction on the property's cost basis and not the fair market value. Sec. 170(b)(1)(C)(iii). However, if the donor elects to deduct the cost basis as a cash-type gift, then all appreciated property gifts and carry forwards from prior years must also be treated as deductible at cost basis. Reg. 1.170A-8(d)(2)(i).

Appreciated Property Gift Annuity for Donor and Spouse

A donor may establish a charitable gift annuity with appreciated property for his or her own life and the life of his or her spouse. With joint or community property, the annuity pays jointly to the two spouses and then to the survivor. In community property states, property held by one spouse may be considered community property if the property was acquired during the marriage or with income earned during the marriage.

If there is any question about title, the common practice is to document the transfer of the appreciated stock into joint or community property prior to funding the gift annuity. If a donor and spouse establish a joint and survivor annuity with joint or community property, no gift tax is due.

The capital gain on the appreciated property will be apportioned between the gift and the contract value. The contract value capital gain will be prorated over the joint life expectancy. If one spouse lives past that expectancy and all gain has been recognized, future payments will be ordinary income.

Successor Gift Annuity Interest

A donor also may establish a successor interest annuity for a spouse using the donor's separate appreciated property. Such an annuity provides an income stream to the donor for life, then to the non-donor spouse for life. In this case, there is no gift tax if the donor retains a right of revocation over the spouse's income stream. No marital deduction is allowed because the non-donor spouse does not have the immediate right to receive income from the annuity. Reg. 25.2523(f)-1(c)(2). To receive a marital estate tax deduction, the donor spouse should retain the testamentary right to revoke the non-donor spouse's income stream. If the donor spouse chooses not to revoke the interest of the surviving spouse in his or her will, the estate may claim a marital estate tax deduction for the value of the income stream. Reg. 20.2056(b)-1(g).

The capital gain will be prorated solely over the donor's life expectancy and, generally, no tax-free income will be distributed until all of the capital gain income has been paid. If there is highly appreciated property, the payments to the first spouse may include no tax-free amounts. All tax-free payments may be to the surviving spouse.

Appreciated Property Gift Annuity for Spouse Created with Separate Property

A donor may also establish a charitable gift annuity solely for a spouse with the donor's appreciated separate property. While this gift model may be appropriate for donors in separate property states, many community property states deem separate property as community property if the property was acquired during the marriage or with income earned during the marriage.

In the case of an annuity funded with separate property and payable only for the annuitant spouse's life, no gift or estate tax is due because of the unlimited marital deduction. Reg. 20.2056(b)-1(g), Example 3; Reg. 25.2523(b)-1(b)(6), Example 3. However, the donor will recognize a portion of the capital gain on the contributed property when the annuity is established. Although the gain allocated to the charitable gift is bypassed, the balance of the prorated gain will be taxable to the donor in the year of the gift. In most circumstances, the tax savings from the charitable gift will offset the tax payable on the capital gain, but the immediate taxation of the prorated capital gain will reduce the net tax savings. The capital gain must be reported on the donor's Form 1040.

Appreciated Property Gift Annuity for Parent and Child

If a parent creates a gift annuity with appreciated property that pays to the parent for life and then to the child for life, the capital gain must be reported during the life of the parent. With appreciated property, the portion of the gain allocated to the charitable gift is bypassed. However, the balance of the capital gain will be reported during the life expectancy of the parent. Once again, the amount reported is limited to the available excluded amount under the exclusion formula. With highly appreciated property, the parent may receive all ordinary income and capital gain, while the child may then benefit from ordinary income and tax-free return of basis.

REAL ESTATE UNITRUSTS AND LIFE ESTATES

A charitable remainder unitrust (CRUT) is an excellent option for donors with appreciated real estate. A CRUT provides a charitable income tax deduction, an income stream and a tax-free sale of the real estate. This tax-free sale of the real estate inside the trust allows the trustee to reinvest the full sale proceeds, providing investment diversification without payment of any capital gains tax.

Because real estate cannot always be sold immediately, a net income plus makeup charitable remainder unitrust (NIMCRUT) or FLIP CRUT is usually recommended. With either type of CRUT, the trustee is not forced to make a trust distribution unless there is actual trust income. A straight CRUT or a charitable remainder annuity trust (CRAT) generally is not recommended when real estate is the only trust asset, because both types of trusts require trust distributions irrespective of actual trust income. In fact, if the trustee does not make the required distributions, the trustee runs the risk of disqualifying the trust.

A popular strategy for real estate is a sale and unitrust plan. With this plan, a donor transfers an undivided percentage of the property into a CRUT and retains the remaining undivided percentage. For example, a donor may transfer 60% of the real estate into the CRUT and retain 40%. After the trust is funded, the real estate is sold and the sale proceeds are divided between the CRUT and the donor in proportion to their ownership interests. This plan is an effective way for a donor to fund a CRUT and receive cash from a single piece of property. Furthermore, in many cases, this plan can provide a zero-tax solution.

Roger Realty Commercial Building

Roger Realty owns a $1 million commercial building. At the age of 70, he is ready to retire from the property management business. Therefore, he is contemplating a sale of the building. Because his CPA took straight line depreciation, Roger's cost basis in the building is only $100,000 and he could have a large tax bill when he decides to sell. Roger would like to sell the property with little or no tax and accomplish some retirement planning as well.

As a result, Roger elects the sale and unitrust option. Based upon his current financial goals, he transfers 70% of the building into a FLIP CRUT. He continues to own the remaining 30% of the building. Four weeks later, the building is sold to a third party for $1 million. The CRUT will receive $700,000 and Roger will receive $300,000.

Because 30% of the building was sold personally by Roger, the $300,000 is subject to capital gains tax. Specifically, Roger will have $270,000 of capital gains ($300,000 - $30,000 prorated cost basis). However, the $700,000 will not be subject to any tax upon sale. In fact, it will generate a $320,000 charitable tax deduction that will produce tax savings to offset all of Roger's $270,000 capital gain. Assuming he can use his charitable tax deduction, this results in a zero-tax sale for Roger. Finally, Roger will receive a lifetime income stream from his $700,000 CRUT and fulfill his retirement planning goals.

Safety Recommendations for Split Gifts

Although hundreds of split gifts are completed annually and the IRS has generally not contested the concept of split transfers, it is prudent to evaluate options that increase the safety of prospective transactions. While no strategy short of a private letter ruling (PLR) for a specific transfer promises 100% safety, several actions may increase safety levels for a split gift.

1. No Personal Use

Trustees must ensure that donors do not have use in any manner of trust property. For personal residences, this means that donors must move out before any portion of that property is transferred to a unitrust.

2. Independent Trustee

Split gifts and self-trustees are an overly aggressive strategy. The IRS in PLR 9114025 repeatedly emphasizes that the "independent trustee acts independently" in order to avoid price manipulation that could increase value received by donors upon sale of their retained interest. Self-trustees who have authority to sell trust assets as trustee and retain assets as owner obviously could manipulate sale terms in a prohibited manner. Independent trusteeship is essential to minimize such potential problems. To reduce risk, a nonprofit or financial advisor trustee is a better option than a donor as trustee.

3. Revocable Trust and Unitrust

An easy method for reducing self-dealing risk is to transfer an undivided interest into a unitrust with an independent trustee and the remaining interest into a revocable trust with that same independent trustee. Donors have the right to income from the unitrust and revocable trust and the right to revoke and recover principal from the revocable trust. However, an independent trustee has both legal title and fiduciary responsibility for both trusts. Given the trustee's ability to control sale terms for both trusts, there is reduced likelihood of a self-dealing violation. In addition, because the trustee has title to 100% of the asset and a fiduciary duty to distribute the sale proceeds in proportionate shares to the unitrust and revocable trust, the donor may be able to take the undiscounted deduction on the CRT (this strategy has not been tested in Tax Court but is based upon sound reasoning).

4. Limited Partnership

Some conservative attorneys might choose to parallel the fact situation of PLR 9114025 by creating a limited partnership. Although undivided interests held in co-ownership would seem to have very similar self-dealing characteristics to a limited partnership, a partnership does indeed fit the specific fact pattern of that ruling.

5. Partial Sale to Charity

Finally, one completely avoids the self-dealing issue by selling the partial interest to a public charity prior to funding the unitrust. After sale of part, the donor transfers the balance of the real property to the charity as trustee of a unitrust. The charity then owns 100% of the asset – part outright and part as trustee of the CRT.

$250,000/$500,000 Home Exclusion

In certain situations, a taxpayer may exclude $250,000 of capital gain (or $500,000 if married) from the sale of taxpayer's principal residence. In order to qualify for this home exclusion, a taxpayer must own and occupy the principal residence for two of the past five years. See Sec. 121. A sale and unitrust plan is an excellent strategy for maximizing a donor's home exclusion, especially since the home exclusion does not have to be prorated between the sale and unitrust. Under this rule, home exclusion can fully apply to the sale portion of the transaction.

Zero Tax Home Sale

Harry and Harriet Homeowner live in a beautiful $1 million home. They purchased the home 30 years ago for $200,000. However, the home is too large for just the two of them. Therefore, Harry and Harriet want to sell their home, downsize to a smaller home, and invest some of the proceeds for retirement. Furthermore, they would appreciate a zero-tax sale solution.

Harry and Harriet qualify for the $500,000 home exclusion because they have owned and occupied the home for two of the past five years. Indeed, they have owned and occupied the home for the past 30 years. However, Harry and Harriet have $800,000 of potential capital gain. In other words, the $500,000 home exclusion would not provide a zero-tax sale, since $300,000 would be subject to tax.

Instead of an outright sale, Harry and Harriet select the sale and unitrust plan. With this plan, they transfer approximately 23% of the home into a unitrust and retain the remaining 77%. With respect to the 23% of the home, or $230,000, Harry and Harriet will bypass up to $184,000 of capital gain, receive a $94,962 charitable deduction and receive lifetime income of approximately $291,443.

Because they retain 77% of the home, or $770,000, Harry and Harriet will receive this amount in cash. This sale is subject to capital gains tax. However, after applying their $500,000 home exclusion and prorating the $200,000 cost basis, Harry and Harriet will have only $116,000 of capital gain to report. Assuming they can use the $94,962 charitable deduction, Harry and Harriet will not owe any tax because the tax savings completely offset the capital gain tax due. Therefore, Harry and Harriet have a zero-tax solution plus the benefits of retirement income and charitable giving!

Debt and CRTs

Mortgaged real estate and CRTs do not mix well together. The transfer of debt-encumbered property into a CRT may trigger two potential problems: 1) grantor trust status which results in disqualification of the trust, and 2) debt-financed income which subjects the CRT to a 100% excise tax on the amount of debt-financed income.

If the debt obligation is solely against the property, the debt is termed "non-recourse." If the obligation is against both the property and the owner personally, the debt is termed "recourse." In most cases, the debt is recourse. The IRS has ruled that the transfer of recourse debt into a CRT will reclassify the trust as a grantor trust. See PLR 9015049. Since a CRT cannot be a grantor trust, the trust will cease to qualify as a CRT. Reg. 1.664-1(a).

If the debt is deemed non-recourse, there is no personal liability under Sec. 677 and, accordingly, no grantor trust status problem. Thus, in the event of non-recourse debt, it may be permissible to transfer the real estate into the CRT without disqualifying the trust.

To avoid a debt-financed income problem to the CRT, it is imperative that even nonrecourse mortgaged property pass the "5 and 5" rule. Simply put, the debt needs to be more than five years old and the property has been owned for more than five years. See 514(c). (For a review of the "5 and 5" rule, see GiftLaw Pro Ch. 2.1.2.) If the 5 and 5 rule is not met, the CRT may have debt-financed income (unrelated business taxable income, or UBTI) upon sale of the property. If this occurs, the CRT is fully taxable. Any trust income would, therefore, be subject to trust tax rates. Accordingly, debt-financed income inside a CRT should be avoided at all costs.

Debt Removal Options

The customary option for real estate with debt is to find a method to transfer unencumbered assets to the CRT. There are at least five solutions to the debt and CRT problem:

Pay Off Debt – If a debt is small, the donor may have resources to pay the debt off and then transfer the real estate to the unitrust.

Release – If there is a parcel of land that may be divided under zoning rules or there are multiple deeds to the parcel, it may be possible to obtain a release on some of the property, leaving the debt on the balance. The released property may then be transferred to the unitrust.

Bridge Loan – The donor may borrow funds on other property, pay off the existing property and transfer an undivided interest into the trust. When the property is sold, the undivided portion retained by the donor is used to pay back the bridge loan.

Charity Purchase – The charitable organization may be willing to purchase part of the real property from the donor. Following this purchase, the donor has funds to pay off the debt and then transfer the balance of the real property into a charitable remainder trust. In many cases, the charity CFO is open to purchasing part of the real property if there is a gift portion. The outright gift of part of the asset reduces the risk for the charity.

Personal Guarantee – While the Service has not approved this method, some counsel have recommended transferring an undivided percentage of encumbered property into a charitable trust. The donor gives a personal guarantee that the trust will not be required to pay debt. When the property is sold, the balance of the asset retained by the donor is used to pay the debt. So long as the transaction works as contemplated, the theory is that the issue is moot after the sale and debt repayment. This is a modestly aggressive strategy and should be taken only after discussions between the donor and his or her professional advisors.

Counsel should consider these five potential steps in order. The technical and practical challenges increase with the latter methods. Nonetheless, given these five options, many donors will find a solution to the debt and CRT problem.

Life Estate in Personal Residence or Farm

A donor may receive a charitable deduction for the transfer of a remainder interest in a personal residence, farm or ranch. Sec. 170(f)(3)(B)(i). The donor deeds the personal residence or farm to a qualified exempt charity and reserves a life estate. The life estate may be a personal right for the donor to use the property, or more commonly a right to the use of the property during the donor's lifetime. The latter option enables the donor to lease the property and receive rental payments during his or her lifetime.

Personal Residence or Farm

A remainder interest may be transferred in any property used by the donor as a personal residence. Personal residence is defined as "any property used by the taxpayer as his personal residence even though it is not used as his principal residence." This may include the taxpayer's vacation or even stock owned by a taxpayer as a tenant-stockholder in a cooperative housing corporation (as those terms are defined in Secs. 216(b)(1) and (2) and if the dwelling which the taxpayer is entitled to occupy as such stockholder is used by him as his personal residence). Reg. 1.170A-7(b)(3).

A remainder interest in a farm also qualifies for a charitable deduction. A farm is property (including the fixtures, buildings, grain bins and other permanent improvements) used by the taxpayer or tenant for the production of crops, fruits, agricultural products or the sustenance of livestock (which includes cattle, hogs, horses, mules, donkeys, sheep, goats, captive fur-bearing animals, chickens, turkeys, pigeons, and other poultry). Reg. 1.170A-7(b)(4). Nearly all property used as a residence or for agricultural purposes will qualify for a life estate gift.

Duration

The qualified transfer of a remainder interest in a personal residence or farm is not subject to any specific limitation on duration in Sec. 170(f)(3)(B)(i), and the Reg. 1.170A-7(b)(3)-(4) specifically mentions retention of an estate for life or term of years. Thus, the transfer can be for a life, lives or a term of years. Since there is no minimum 10% deduction test, such as applies with a charitable remainder trust or charitable gift annuity, there is no specific limit on the number of lives used for the life estate. However, the life estate is most commonly created for one or two lives.

Undivided Interests in Life Estates

It is also possible to transfer an undivided percentage of the remainder interest. For example, a remainder interest in part of a farm may be transferred to charity. Rev. Rul. 78-303. Alternatively, the remainder interest may be divided and a portion of the remainder transferred to family with the balance transferred to charity. Rev. Rul. 87-37. However, if the charity receives a minority interest in the remainder, it is possible that the minority interest should be subject to a valuation discount.

The ability to transfer part of a remainder interest is beneficial if there is debt on the property. It may be possible to combine a remainder interest gift with a bargain sale. Sec. 1011(a). Alternatively, the charity may purchase a portion of the remainder interest sufficient to pay the debt, and the donor may then give the charity the balance of the remainder interest.

ACCELERATING CHARITABLE EFFORTS (ACE) ACT MAY CHILL DONATIONS

The ACE Act would create new restrictions on donor advised funds (DAFs). The attorneys general stated, "The Act's disclosure requirements would cause donors who might otherwise anonymously contribute to a preferred charity through a DAF to not donate at all. This harms not just the donor, but the charity itself."

DAFs enable individuals to receive an immediate tax deduction and recommend grants. This is "an attractive option to maximize their charitable giving." Public charities often allow anonymous DAF contributions and use these gifts to show that they have the required broad public support. Under current law, private foundations may also contribute to a DAF and fulfill their required 5% annual distribution.

The letter stated that the ACE Act will "chill donations and frustrate the ability of charities to receive funding." It would prohibit public charities from using anonymous DAF donations to fulfill the public-support test. Only if individual donors are named will charities be able to use the DAF gifts to satisfy this test.

The attorneys general believe that there are many "sound reasons why donors may wish to remain anonymous." These may include religious beliefs, modesty or concern that the charity is considered controversial by other individuals. The disclosure requirements proposed in the ACE Act may cause donors who would otherwise contribute anonymously to refrain from making any gifts. The letter's authors believe the ACE Act's mandatory disclosure provision harms both the donor and the charity.

In addition, private foundations would be damaged, the letter suggested. If a private foundation is not able to make a gift to a donor advised fund and count that as part of its 5% mandatory distribution, there will be fewer gifts to DAFs.

The attorneys general conclude, "While these proposed changes are likely to chill charitable giving, there is no indication that they further any public good or prevent abuse."

These attorneys general are concerned about protecting the privacy of citizens. In their view, the right to make anonymous charitable gifts is an important element of that privacy. Therefore, the 14 attorneys general oppose the ACE Act and suggests that it would harm donors and nonprofits.

Editor's Note: The 14 attorneys general view their role as advocates for privacy rights. They are concerned that the ACE Act would reduce the privacy right of donors to make anonymous contributions.

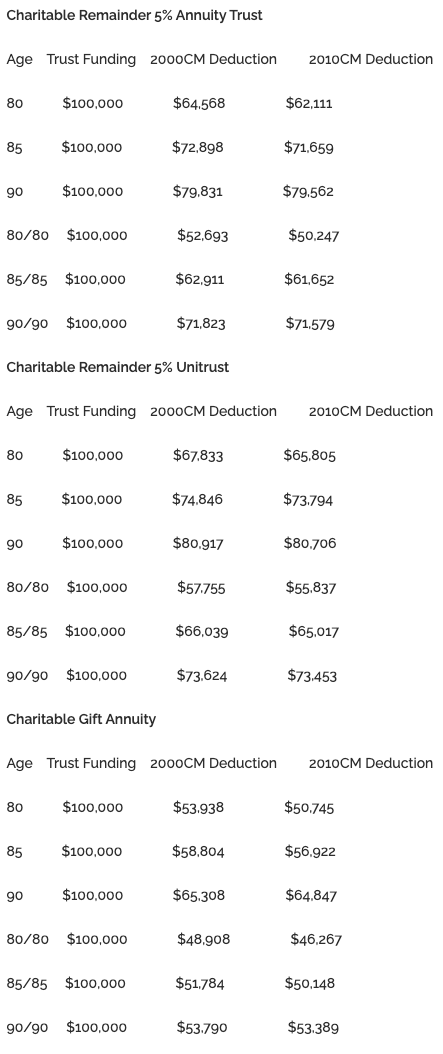

UPDATED IRS CHARITABLE DEDUCTION TABLES

In REG–122770–18, the IRS published new "Actuarial Tables and Valuing Annuities, Interests for Life or a Term of Years, and Remainder or Reversionary Interest."

Under Section 7520, the IRS is required each 10 years to publish new mortality tables that are used to value annuities, interests for life or a term of years and remainder or reversionary interests. The latest tables are based on the 2010 census and are titled "2010CM."

The proposed regulations include the new 2010 CM mortality table and will be effective on the first day of the month after the regulations are made permanent. There is a 60-day comment period that concludes on July 5, 2022. Following that comment period and an opportunity for further IRS review, the final regulations will be promulgated. Deduction calculations on or after the first day of the next month must use the 2010CM mortality table.

Section 7520 generally requires the use of the most recent mortality tables and an interest rate that is 120% of the Federal midterm rate under Section 1274(d)(1) for the month of the valuation. If a charitable contribution is allowable, the taxpayer may elect under Section 7520(a) to use a Federal midterm rate for either of the two months preceding the month before the valuation date.

The actuarial tables based on 2010CM are available at https://www.irs.gov/retirement-plans/actuarial-tables. This IRS webpage includes both the existing tables using 2000CM and the new tables. The new tables will update the deduction calculations based on longer life expectancies. The new mortality tables will impact Table S (Single Life Remainder Factors), Table U(1) for unitrust single life factors and Table U(2) for two life unitrust factors.

The proposed regulations include transition rules. If a valuation is completed on or after January 1, 2021 and before the applicable date for the tables as published in final regulations, a donor may elect to use either the 2000CM or 2010CM mortality tables. If a donor passes away during that same period, the election is also permitted. After the final regulations have established the fixed date for the new tables, all deduction calculations thereafter must use the Table 2010CM factors.

If a decedent was under a mental disability, an executor was previously permitted to use the tables effective on the date of the disability to conduct calculations. This rule is now changed. The IRS noted, "A special rule permitting an election to use the interest rate in effect at the time the decedent first became subject to the metal disability is not necessary. The same is true with respect to mortality rates." Therefore, all estates will be required to use the interest rate and mortality table in effect on the date of death.

Editor's Note: The field of philanthropy has been waiting for the tables to be published. Because the IRS is required by law to comply with the comment requirement, it is probable the effective date of the new tables will be during the second half of 2022. With longer expectancies, deductions for life income agreements will generally be lower with the new tables, so few donors will elect to use them before the mandatory date.

Reduced Charitable Deductions with New IRS Tables

When the REG–122770–18 proposed regulations for "Actuarial Tables and Valuing Annuities, Interests for Life or a Term of Years, and Remainder or Reversionary Interest" are made final, the values of charitable deductions for annuity trusts, unitrusts and charitable gift annuities will be lower.