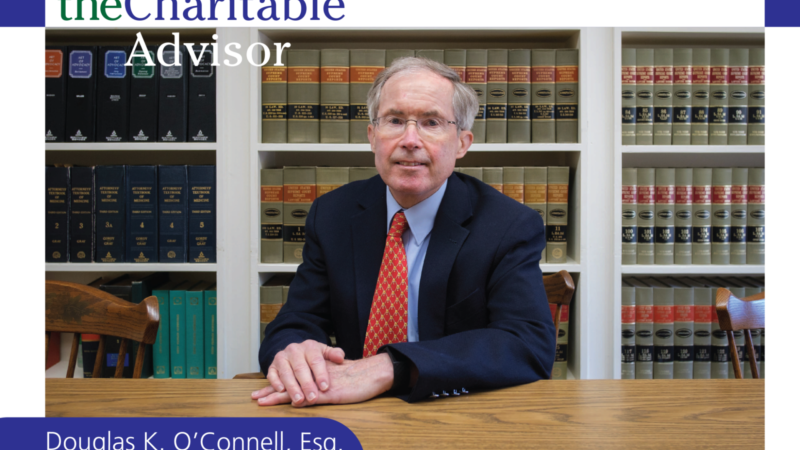

An Interview with Attorney Douglas K. O‘Connell, Esq.

The Community Foundation recently sat down with Douglas K. O’Connell, Esq. of Howd, Lavieri & Finch, LLP, one of Northwest Connecticut’s oldest and most established law firms, to discuss options for effective planned giving.

An Interview With Attorney Douglas K. O‘connell, Esq.

The Community Foundation recently sat down with Douglas K. O’Connell, Esq. of Howd, Lavieri & Finch, LLP, one of Northwest Connecticut’s oldest and most established law firms, to discuss options for effective planned giving.

NCCF: Tell us about the relationship between estate planning and charitable giving.

DO: Estate planning is a significant part of my practice. It involves advising clients on how best to get their affairs in order for when they pass and assisting clients as they decide how best to leave the assets they have amassed over their lifetime. Planned charitable giving is a common conversation that I have with couples and individuals who don’t have any direct heirs or whose children are well off. In other instances, clients are concerned that an inheritance could do certain family members more harm than good. In those situations, the question clients often ask is: “Is there a better use for our money?” or “Should we leave our estate to relatives we seldom see?” In response to those questions, I typically introduce the concept of charitable giving as a solution. There are also clients who come to me who have already decided to give a portion of their estate to charity. Through life experiences, or their connections to their community. Some clients even know exactly which charities they would like to support.

NCCF: What are some concerns you address with your clients related to charitable giving?

DO: When I have clients who want to give a large gift to a specific charity, I encourage them to consider whether or not that charity has the resources to manage a large gift. Most charities are in the business of providing a service, not managing an inheritance. Some of the most effective local charities are managed by a small team of staff and/or volunteers efficiently and effectively focused on their missions. Establishing a designated or field-of-interest fund at a community foundation enables my clients to benefit local charities without burdening them with financial and investment management.

NCCF: What are some popular vehicles for charitable giving?

DO: Charitable Remainder Trusts remain a popular and viable tool for some clients. These trusts typically provide for payments to an individual for a specific period of time, or even life. Once that period has ended, the principal trust balance benefits a specific non-profit. We also work with clients to make direct charitable gifts to a community foundation, such as the Northwest CT Community Foundation. Establishing an endowed or non-endowed donor-advised, designated, and/or field-of-interest fund that can benefit one or many charities or areas of need can be an effective vehicle for those who are charitably inclined. Private foundations are another vehicle, though not a vehicle I typically recommend anymore. I am not aware of many attorneys who recommend them.

NCCF: You mentioned that you don’t often recommend clients establish a private foundation. Can you tell us more about that?

DO: Establishing a fund at a community foundation that meets the charitable goals of the client is almost always more cost-effective when compared to establishing a private foundation. Some clients still prefer a private foundation. But, by and large, clients who come in thinking they want to establish a private foundation, usually decide to establish a donor advised fund with a community foundation instead. The smaller the charitable gift amount, the less sense a private foundation makes. Even with larger gifts, it is difficult for a private foundation to duplicate the services available through a community foundation—investment oversight, community knowledge, skilled grants staff, technology systems, and succession planning— in a cost-effective manner. Successorship is also a huge issue. The question must be asked: “Who is going to manage the private foundation when the client or other immediate successors are gone?” Successorship is often a driving factor in terms of people steering away from private foundations. When no viable successors are available, one common solution is to transfer the private foundation assets to a community foundation fund, either as a donor-advised fund or as field-of-interest or discretionary fund. The community foundation Board of Trustees will then continue to award grants in the name of the fund indefinitely.

2021 Charitable Contribution Opportunities

In early 2020, the economy saw a sharp decline as the coronavirus began to spread throughout the United States. Shortly thereafter, the Coronavirus Aid, Relief, and Economic Security (CARES) Act was enacted to aid the nation's economic recovery. In part, this bill set forth temporary changes to encourage charitable giving during this challenging period. A number of these changes were extended through 2021 by the Consolidated Appropriations Act (CAA).

This article details the charitable deduction changes introduced by the CARES Act and extended through 2021 by the CAA. The discussion will focus on the above-the-line charitable deduction for non-itemizers and the increased deduction limits for cash and food inventory gifts to charity.

Individuals may claim charitable income tax deductions for certain types of contributions made to qualifying charitable organizations. Charitable income tax deductions are subject to certain deduction limits, based on the donor's taxable income, the type of asset donated and the nature of the recipient organization. For donors to reap the tax benefits of charitable income tax deductions, donors must itemize their deductions. Otherwise, donors are usually limited to the standard deduction.

Under the Tax Cuts and Jobs Act (TCJA), effective in 2018, the standard deduction increased to almost double its prior value and eliminated some itemized deductions. Since the passage of the TCJA, only about 10% of taxpayers itemize their deductions.

Above-the-Line Charitable Deduction for Cash Gifts

The CARES Act introduced a $300 charitable deduction for cash gifts made by non-itemizers filing individually or jointly in 2020. This "above-the-line" charitable deduction enables the majority of taxpayers who take the standard deduction to also benefit from their charitable gifts of cash. The CAA extended the $300 deduction for individuals through 2021 and increased it to $600 for joint filers making cash gifts to charity.

For purposes of this limit, qualified organizations are those described by the IRS as Sec. 170(c) organizations, with a few exceptions. Examples of qualified organizations include churches, educational institutions, hospitals, publicly supported charities and private operating foundations. Cash contributions to supporting organizations, donor advised funds, charitable remainder trusts and certain types of private foundations do not qualify for the above-the-line charitable deduction. See IRS Publication 526 for more information on the types of organizations that may qualify.

Eligible contributions must be made by cash or check. Cash contributions do not include the value of volunteer services, securities, household items or other property. Contributions carried forward from prior years do not qualify for the above-the-line deduction.

Example:

Tom and Jane are married, file their taxes jointly and take the standard deduction. In 2020, Tom and Jane gave a total of $500 in cash to their favorite charity. Under the CARES Act, Tom and Jane can deduct up to $300 by using the above-the-line charitable deduction.

In 2021, Tom and Jane decide to double their impact on their favorite charity by donating $1,000 in cash. They will be able to deduct up to $600 of this contribution under the CAA's increased benefit for married couples filing jointly. They will not be able to carry forward the remaining charitable contribution amounts in either year.

In 2020 and 2021, Tom and Jane also contributed $1000 in cash to their donor advised fund (DAF). Their advisor informs them that DAF gifts cannot be counted toward the above-the-line deduction, although DAF gifts are eligible for an itemized deduction.

This above-the-line deduction available through 2021 allows taxpayers to deduct their modest cash gifts without needing to itemize their deductions. For those wishing to contribute larger amounts and willing to itemize deductions, expanded giving opportunities are available.

100% Charitable Deduction Limit for Cash Gifts

In most years, the charitable deduction limit for cash gifts is limited to 60% of a donor's adjusted gross income (AGI). Gifts in excess of the applicable deduction limits may be carried forward for up to five additional years. Under the TCJA, the deduction limit for cash gifts to qualifying organizations was increased from 50% of the donor's AGI to 60%. Under the CARES Act and CAA, individuals can elect to apply up to 100% of their AGI in 2020 and 2021.

To be deductible under this increased limit, qualified contributions must be made in cash or by check to a qualified charitable organization and the donor must elect to use the enhanced charitable deduction limit. Cash contributions to DAFs, supporting organizations and charitable trusts do not qualify for this increased individual deduction limit.

The election to use the increased individual limit is made on a contribution-by-contribution basis. The donor must make the election for each qualified contribution, otherwise the usual percentage will limit apply. The election must be made on the donor's IRS Form 1040 or IRS Form 1040-SR. It is important to note that any of the donor's other types of charitable deductions, such as those for gifts of appreciated property or to a DAF, will reduce the maximum amount allowed under this election.

Example:

Daniel is employed as an electrical engineer and expects an AGI of $150,000 this year. In 2021, he receives an inheritance of $1,000,000 in cash from his late aunt's estate. He contributes his entire salary to his favorite public charity to establish a summer camp program for children in need. Due to the increased individual limit, Daniel may deduct this gift in its entirety. Assuming Daniel's $150,000 AGI places him in the 24% income tax bracket, this gift may save up to $36,000 in income taxes.

25% Charitable Deduction Limit for Cash Gifts from Corporations

For Subchapter C corporations, the usual deduction limit for cash gifts is 10% of taxable income for donations made to public charities. For 2020 and 2021, corporate cash gifts are deductible up to 25% of taxable income. As with the increased individual limit, the corporation must elect to use the increased corporate charitable deduction limit on a contribution-by-contribution basis.

Example:

Three years ago, avid bakers Joseph and Ernest started Bagels, Inc., which is organized as a C corporation. The company has been wildly successful from the start. The company regularly contributes $50,000 in cash each year to support its local food bank. The goal has been to donate approximately 10% of the company's taxable income, which usually reflects the maximum deductible percentage for corporate charitable cash gifts.

This year, Joseph and Ernest have been thankful for a steady stream of business, but they have seen their community particularly impacted by business closures. Bagels, Inc. plans to take advantage of the increased corporate limit by making a generous cash gift to the local food bank of $100,000. Assuming the business' taxable income of $500,000 remains consistent for 2021, Bagels, Inc. could potentially donate up to $125,000 this year and deduct this amount in full.

Increased Deduction Limit for Certain Food Inventory Gifts

Certain donations of food inventory for the ill, needy, and infants are eligible for enhanced deduction limits. For 2020 and 2021 contributions, the limit for this type of deduction is increased from 15% to 25%. For C corporations, this percentage limit is based on taxable income. For other entities or individuals, the limit is based on the aggregate net income for the trades or businesses from which the contributions were made. The organization receiving the food donation may not be a private nonoperating foundation.

The IRS worksheet "Donations of Food Inventory" provides guidance on calculating the food inventory charitable deduction. The donor must first determine the fair market value (FMV) of the donated food by identifying the price at which the food would normally be sold. The donor does not reduce the FMV because the donated food item did not sell or because the food was prepared specifically for donation and not resale.

Next, the donor must determine the basis of the donated food. If a business does not account for inventories and is not required to capitalize indirect costs, it may elect to treat the basis of the food as being 25% of its FMV.

If the basis of the donated food is the same as or exceeds the FMV, the donor may claim a charitable deduction for the FMV of the donated food. If the FMV exceeds the basis, then the worksheet will lead the donor through a series of calculations to arrive at the charitable deduction. The charitable deduction will be the lesser of twice the basis of the donated food or the basis of the food plus one-half of the expected profit if sold at FMV.

Example:

Tony's Market receives a new shipment of dairy products every other week. The company then donates the remainder of the previous shipment's unexpired dairy products to the local women and children's shelter, a public charity, to stock their food pantry. The shelter provides Tony's Market with written confirmation that the donated dairy products will not be sold or exchanged in any way for value and will only be used to support their purpose of feeding the needy. The donated products must comply with the requirements of the Federal Food, Drug, and Cosmetic Act in effect on the gift date and as applicable for the prior six months.

For its first contribution of 2021, Tony's Market donates 20 gallons of milk. The basis in each gallon of milk is $1 and the FMV is $4. The company's CPA advises that Tony's Market may potentially deduct up to $2 for each gallon donated. This deduction reflects the lesser of twice the basis of each gallon ($1 x 2 = $2) or the basis plus one-half of the expected profit ($1 + $1.50 = $2.50).

The CPA notes that since Tony's Market is organized as a C corporation, it can potentially deduct up to 25% of its taxable income through charitable contributions of food inventory.

Conclusion

The CARES Act and CAA have broadened opportunities for philanthropy in 2020 and 2021. For individuals, one of the simplest ways to give is to make a cash donation and take advantage of the above-the-line charitable deduction. For donors choosing to itemize their deductions, now is an opportune time to give generous cash gifts in an amount up to 100% of their AGI.

Corporations can also fulfill their charitable goals by taking advantage of the increased deduction limit of 25% for cash gifts. Finally, both individuals and businesses wishing to make immediate and tangible gifts may deduct up to 25% of their aggregate net income through qualifying food inventory gift.

Charitable Gifts of Real Estate - Part 1

For many donors, the most significant part of their net worth is real estate. Thus, gifts of real estate are a very common asset used for charitable gifts. As a general rule, many charities prefer gifts of cash, stocks and bonds because these types of gifts are easy to transfer, value and liquidate. In contrast, gifts of real estate may bring legal and financial liability that gives rise to numerous issues the charity must navigate.

Real estate is a unique asset and each gift must be properly tailored to the property and the donor's expectations, while protecting the charity from any issues that may arise. Charities and donors must ensure they are well equipped and informed about the benefits and pitfalls of gifts of real estate.

This series about gifting real estate will discuss the definition of real estate, charitable deductions for real estate gifts, charitable gift options and some best practices. This first article will touch on overarching considerations from a donor's and charity's point of view when gifting real estate.

Introduction

There are a variety of categories of real estate, including residential property, commercial property and agriculture. Real property comes in many forms—homes, office buildings, undeveloped lots and timber land are a few examples. Generally, the best property for a donor to use as a charitable contribution is unencumbered real property that has been held for longer than one year.

Without any charitable gift, the sale of real estate will trigger income for the owner. Generally, the owner will owe taxes on the income gain resulting from the sale—the excess of the sale price over the cost basis of the property. Gifts of real estate to a charity satisfy the donor's charitable purposes, as well as offer a charitable deduction and bypass capital gains. The gift may include lifetime payouts and other benefits.

Considerations When Gifting Real Estate

i. Deduction Limitations

The donor's charitable deduction is based on two factors. First, the property must qualify as a capital asset. Real estate that is inventory or sold in the ordinary course of the donor's business is not a capital asset and is instead treated as an ordinary income asset. Personal residences generally qualify as capital assets. If the real estate does not qualify as a capital asset, the donor's charitable deduction is limited to the cost basis.

Second, the charitable deduction is dependent on whether the property is classified as a long-term capital gain asset or a short-term capital gain asset. A long-term asset is one that the donor holds for more than one-year, while a short-term asset is held for less than a year. If the gift is a long-term asset, the donor may be entitled to a charitable deduction equal to the fair market value (FMV) of the real estate. However, gifts of a short-term asset or an inventory-type asset are only deductible at cost basis.

Generally, the donor's charitable deduction for gifts of appreciated property (including real estate) is limited to 30% of the donor's adjusted gross income (AGI), with a potential carry forward up to five additional years. This limitation may disallow a donor from taking the entire charitable deduction amount in year one, but the five-year carry forward gives the donor the opportunity to take the entire amount spread out up to six years.

The donor may elect to deduct the cost basis of appreciated property at 50% of his or her AGI. This is a helpful option for a donor who desires to make a large gift of real estate that has a high basis. The higher 50% of AGI deduction limitation may allow the donor to take the entire deduction in the year of the gift, rather than needing to carry it forward. However, if the donor elects to deduct at cost basis, then all other appreciated property gifts and carry forwards must also be deducted at cost basis.

The CARES Act increased the deduction limitation for cash gifts in 2020 to 100% of the donor's AGI. However, there is not a change in the deduction limitation for gifts of appreciated property, which includes real estate.

ii. Partial Interest Gifts

In general, the donor is not eligible for a charitable deduction when gifting a partial interest. There is an exception for giving an undivided fractional interest in property. An undivided fractional interest in property is an undivided portion of a donor's entire interest in property, which qualifies for a charitable deduction when gifted to a charity. See the partial interest gift examples below.

Example 1

Fred owns land with mineral deposits. He is considering a gift to his favorite charity. Fred asks his advisor about making a gift of the land, while retaining the mineral rights. His advisor explains that structuring the gift this way would be a gift of a partial interest and is not eligible for a charitable deduction. Furthermore, in order for Fred to receive a charitable deduction, he must give an undivided interest in the land and the mineral rights. His advisor asks him to consider an alternative arrangement, Fred can meet his philanthropic goals by making a gift of a 25% undivided interest in the land and the mineral rights. While it is only a portion of the property, it is a deductible interest. Fred is very pleased that his gift can make a lasting impact at his favorite charity.

Example 2

Mary has a home that she is thinking about selling and she would like to donate some of the sale proceeds to charity. She considered a cash gift to charity out of the proceeds of the sale, but realized she would need to pay capital gains taxes on the sale. She asked her advisor for guidance on the best route. The advisor recommends Mary gift a 50% interest in the home to charity, retain the other 50% interest and sell the property in a gift and sale arrangement. She asks if she would be eligible for a charitable deduction on the 50% interest gifted. The advisor explains that the gifted 50% interest qualifies as an undivided fractional interest and she is eligible for a charitable deduction. Mary is also only taxed on the gain for her 50% portion of the home, rather than capital gains on the entire gain in the sale of the home. Mary is pleased with the advisor's plan and proceeds with the gift arrangement.

Professional advisors should understand the difference between a partial interest gift and an undivided fractional share when helping donors with real estate gifts. The goals of the donor may vary and care should be taken when a donor intends to make a donation that will generate a charitable income tax deduction.

iii. Gift Acceptance Policies

The gift acceptance policy of an organization may dictate the parameters for acceptance of a charitable contribution from a donor. Generally, there are three categories of gift acceptance policies a charity may implement. Certain types of gifts, such as real estate, may fall under exceptions to the standard acceptance parameters and need to be approved on a case-by-case basis.

When a charity creates real estate gift acceptance policies, it must consider the Comprehensive Environmental Response, Compensation, and Liability Act of 1980 (CERCLA). Under CERCLA, the current property owner (i.e. a charity) or anyone in the chain of title can be held liable for cleanup costs, even if they are not responsible for any of the property contamination. When a charity accepts a gift of real estate, it will have taken title to the property and can be held liable under CERCLA. The potential for unlimited liability under CERCLA requires a charity's decision to accept gifts of real estate to be done carefully and with due diligence. It is highly recommended that the charity create a gift acceptance policy that best suits the charity's tolerance for risk and reward.

Some charities will adopt a "no acceptance" policy based upon the potential environmental liabilities under CERCLA. The policy is simple—all gifts of real estate will be rejected. Although the charity is ensured it will not inherit any liabilities associated with real estate ownership, the charity is limiting its charitable gifts. Accordingly, fewer charitable gifts mean less money for the charity. Considering that many donors' wealth is in real estate, a blanket "no acceptance" policy would deny these donors from achieving their philanthropic goals along with reducing the amount of gifts to the charity.

On the opposite end of the spectrum is the "accept everything" policy. This policy is not necessarily formally adopted, but is a result of a lack of careful planning. A charity in this position often will not have a formal gift acceptance policy or lacks a committee to review proposed gifts. The benefit of this policy is that the charity can receive more charitable gifts, but the downside is the charity might unknowingly accept gifts of real estate with environmental risk and liabilities that far exceed its value. The uniqueness of the benefits and liabilities of real estate makes an "accept everything" policy unsuitable for charities.

The middle ground is the "case-by-case" acceptance policy. This policy understands the uniqueness of real estate and the risks and rewards associated with each gift of real estate. A charity's gift acceptance policy should be designed to accept "good" gifts, while rejecting "bad" gifts. A flexible gift acceptance policy on a "case-by-case" basis is the ideal approach for many charities. It reduces liabilities, while enhancing donor contributions and gift options.

iv. Environmental Factors

Real estate gifts may come with heightened risk factors compared to other types of property. Although the charity will attempt to sell the real estate as soon as possible, once in the chain of title any environmental issues may subject the charity to liability.

Charities must carefully review each gift of real estate before acceptance, but may need to take additional steps if the real estate is commercial or industrial in nature. Commercial or industrial real estate is more likely to have issues with hazardous materials incurring CERCLA liability than a typical residential property.

As an additional step, charities can obtain an environmental impact survey (EIS) to assess the potential environmental risks associated with the property. There are three levels of testing: Phase 1, Phase 2 and Phase 3. With each higher phase the charity is provided with more assurances regarding the likelihood of the potential environmental issues, but the higher phases have increasing costs. There are no tax rules that regulate who pays for the EIS costs. The charity and donor are free to negotiate the costs.

As is true with all gifts of real estate, the charity must consider the risks and rewards of accepting the gift. A "good" gift of real estate with unknown environmental issues can create significant problems for a charity. Therefore, charities must ensure all steps are taken to identify and determine the environmental issues before acceptance.

v. Mortgaged Real Estate

Potential gifts of real estate may be encumbered by a mortgage. Encumbered real estate is not ideal for charitable contributions. When encumbered real estate is gifted, the debt remains on the property, unless it is paid off. If a donor wants to gift debt-encumbered property, the charity should consider several factors before accepting the gift.

The charity may choose to "step into the shoes" of the donor and make payments on the mortgage prior to the sale of the property. Because the charity acquires the property subject to a recorded mortgage, the gift is treated as a bargain sale. The donor's relief of indebtedness is treated as gain to the extent the debt exceeds the cost basis. The donor will only receive a charitable deduction for the equity portion of the gift. In short, the charitable deduction will be reduced by the value of the debt on the property. The charity does not assume the mortgage, but may make payments to protect its interest in the property.

One very important consideration is that mortgaged property may be categorized as "acquisition indebtedness" property under Sec. 514(c)(2)(A). When a charity acquires property subject to a mortgage or other similar lien, the amount of the indebtedness is considered to be the indebtedness of the organization incurred in acquiring such property. This designation occurs regardless of the organization assuming or agreeing to pay such indebtedness. If the charity is subject to acquisition indebtedness when encumbered property is acquired, the charity may owe unrelated business income tax (UBIT) upon the sale of the property.

However, there is one exception to the acquisition indebtedness rule under the "Five and Five" exception. This exception allows a safe harbor if the debt has been on the property for more than five years and the donor has owned the property for more than five years. Sec. 514(c)(2)(B). If the exception applies, the charity receives the property free of acquisition indebtedness for a period of ten years. Therefore, if the property passes the "Five and Five" test, then the charity may receive and sell the property within the ten-year period without payment of UBIT. This exception may not apply to many properties, especially in a low interest environment where many property owners will refinance debts.

There is one important pitfall within the "Five and Five" exception for the charity to avoid. The charity must receive the property subject to the debt, but may not assume the debt obligation. That is, the charity may receive title and make payments on the debt to defend its position and title, but it must not contractually obligate itself with the lender to pay the indebtedness secured by the mortgage.

There are several steps that may be undertaken prior to accepting the gift of real estate. If the "Five and Five" exception does not apply, the donor should be encouraged to pay the debt on the property prior to making the donation. There are multiple strategies to enable the donor to pay off the debt, which may include a bridge loan or working with a lender to release the debt. If the donor gifts indebted property, the charity may avoid UBIT by paying off the debt and then holding the real estate for 12-months before selling it. However, some nonprofits may lack the financial resources for this strategy.

If the donor gifts debt-encumbered property to charity, the donor's equity in the property will generate a charitable deduction, but the amount of the mortgage will be treated as a "release of indebtedness" to the donor. This release of indebtedness is a taxable event. The amount of debt the donor is relieved from paying must be reported by the donor as capital gain in the year of the gift. The donor's charitable deduction may offset some or all of the taxes due. The offset of capital gains tax is an important consideration to note when speaking to donors about gifts of debt-encumbered property.

When gifting real estate, the charity must ensure the donor is aware of any encumbrances on the property and the potential associated issues. Additionally, the donor needs to be informed of the effect of transferring encumbered real estate to charity.

vi. Charitable Deduction Substantiation

Donors who make real estate gifts must file IRS Form 8283 with their tax return, which applies to all non-cash charitable contributions greater than $500. Under Reg. 1.170A-16(d)(1)(ii), donors must also obtain a contemporaneous written acknowledgment from the charity for the charitable contribution. Additional requirements may apply based on the value of the property.

In general, the IRS requires a qualified appraisal for gifts of non-cash assets to charity that exceed a value of $5,000. This requirement applies to gifts of real estate. To be considered a qualified appraisal, it must not be performed earlier than 60 days prior to the date of the transfer and must be obtained prior to the due date, including any extensions, of the tax return on which the charitable deduction is claimed. If the property is valued in excess of $500,000, the donor is required to attach the qualified appraisal to the tax return for the year of the gift, in addition to Form 8283. Reg. 1.170A-16(e)(1)(iv).

Although required by the IRS, a qualified appraisal is also used to determine the fair market value (FMV) of the gifted real estate. If the gift is a long-term capital asset, the FMV determined from the qualified appraisal should be used to calculate the donor's charitable deduction.

The majority of real estate gifts are in excess of $5,000. Acquiring a qualified appraisal is an absolutely essential aspect of gifts of real estate to charity. Without a qualified appraisal, the IRS may deny the donor's charitable deduction.

vii. Depreciation

In many cases, a donor may wish to gift real estate that he or she has depreciated over time, such as rental property. Donors must be aware of the impact depreciation can have when gifting real estate to charity. Accelerated depreciation recapture on improvements can decrease the charitable deduction.

If the donor gifts property that was depreciated using the accelerated depreciation method, the donor may need to reduce the charitable deduction by the ordinary income portion of the asset value. The excess of the accelerated depreciation over the straight-line method would be ordinary income if the asset were sold. Because the ordinary income portion of value is not deductible under Sec. 170(e)(1)(A), a gift of property that has been subject to accelerated depreciation to a charity will lead to a reduced deduction.

viii. Prearranged Sale

A prearranged sale occurs when there is an identified purchaser, an identified price and a legally enforceable agreement to sell the property before the real estate is gifted to charity. If a prearranged sale occurs, the donor forfeits any bypass of capital gain and must realize the income gained in the transfer to charity.

In Rev. Rul. 78-197, the IRS established a bright line test to determine a prearranged sale. When a charitable gift is followed by a "prearranged redemption" or "pursuant to a prearranged plan" the IRS will "treat the proceeds as income to the donor." The rule on prearranged sales is rooted in contract law. If the contract has proceeded to a point when performance can be compelled, then a binding agreement exists.

A major benefit of gifting real estate to charity is the bypass of capital gain. The charity and donor must be cognizant that a prearranged sale will forfeit the donor's bypass of capital gain.

Conclusion

There are many issues to consider when gifting real estate to charities. These issues can limit or disqualify a donor from receiving a charitable deduction or can seriously impact a charity that accepts the wrong types of real estate gifts. Despite the risks and intricacies of real estate gifts, donors and charities can effectively navigate real estate gifts with careful planning and thoughtfulness. These gifts can be structured to maximize the benefits for both the donor and the charity. November's Article of the Month will discuss different ways to structure real estate gifts to charity.

Bipartisan Conservation Act May Impact Charitable Deductions

On September 13, the House Ways and Means Committee released a summary of the tax provisions from the Build Back Better bill. One of the included tax provisions is the Charitable Conservation Easement Program Integrity Act (CCEPIA).

CCEPIA would deny a charitable deduction for a conservation easement if it exceeds 2½ times the taxpayer's basis. However, there would be exceptions if the taxpayer holds the interest for three years or the donation is by a family partnership. The deduction disallowances are intended to discourage syndicated partnerships from taking inflated deductions for conservation easements. If a syndicated partnership easement deduction is disallowed, there would also be a gross valuation misstatement and an increase in the penalty from 20% to 40% of the tax underpayment.

The Ways and Means provision includes an additional exception for many taxpayers. If the IRS denies a conservation easement charitable deduction, most taxpayers would be permitted to correct defective easement grants within 90 days. The exception would not apply to syndicated partnerships.

Both supporters and opponents of the conservation deduction provision commented on the inclusion of CCEPIA in the BBB Act. Lori Faeth of the Land Trust Alliance stated, "We do not have any indication that the legislation would be removed from the reconciliation bill."

The Partnership for Conservation opposes the Ways and Means provision. It criticized the December 23, 2016 retroactive date of the measure. This is the date when Notice 2017-10, 2017-4 IRB 544 was released and designated a syndicated conservation easement as a listed transaction.

Robert Ramsey, president of the Partnership for Conservation, stated, "Members of Congress must recognize the profound injustice and dangerous precedent that would be imposed by setting punitive retroactive tax policy and strip this misguided proposal from any final legislative package."

The Land Trust Alliance indicates that the retroactivity complaint should not stand. The syndicated conservation easement organizations were warned in Notice 2017-10 that the IRS would be scrutinizing these deductions.

Editor's Note: There are a number of conservation organizations that believe CCEPIA will protect future conservation easement deductions by limiting the large deductions previously taken by syndicated partnerships. The debate will continue whether to include this provision in the Build Back Better Act.

Expanded Tax Benefits for 2021 Gifts

In a September 17 letter, the Internal Revenue Service explained how both individuals and businesses may receive additional benefits for charitable gifts this year. The Taxpayer Certainty and Disaster Tax Relief Act of 2020 included four temporary tax benefits to encourage charitable gifts. These benefits include deductions for individuals who do not itemize, a 100% AGI limit for itemized charitable cash gifts by individuals, increased corporate charitable deductions and increased limits for businesses that donate food inventory.

1. Non-itemizer Taxpayers — Because the Tax Cuts and Jobs Act of 2017 dramatically increased the standard deduction, almost 90% of taxpayers do not itemize. At one time, taxpayers who did not itemize could not use the benefits of a charitable deduction. However, for 2021, the CARES Act made it possible to deduct cash gifts up to $300 for an individual or $600 for a married couple filing jointly. These additional deductions are available for taxpayers who take the standard deduction.

There are some limits on the $300 or $600 deduction for nonitemizers. Gifts must be cash and made to a qualified public charity. These gifts may not be to a donor advised fund, most private foundations or charitable remainder trusts. Gifts of cash include those made by check, credit card or debit card. Volunteers who have unreimbursed out-of-pocket expenses will also qualify for this deduction.

2. Cash Deductions Up to 100% AGI — In recent years, cash gifts to public charities have deduction limits of 60% of a donor's adjusted gross income (AGI). Donors who contribute more than the 60% limit may carry forward the deduction for up to five years after the year of the gift.

The limit for cash gifts made in 2021 is temporarily expanded to 100% of AGI. Once again, there are some special rules. These gifts must be in cash and may not be to a donor advised fund, supporting organization or charitable remainder trust. Taxpayers must make an election on their IRS Form 1040 to use the 100% of AGI deduction limit.

3. Increased Corporate Deductions — Large corporations are typically structured as "C" corporations. They usually have a limit for charitable gifts of 10% of taxable income. However, for 2021, C corporations may donate up to 25% of their taxable income. The gift must be a cash gift and elected on the corporate tax return.

4. Donations of Food Inventory — C corporations are permitted to take an enhanced deduction for gifts of food inventory for the benefit of the ill, needy, and infants. In 2021, the deduction limit is increased from 15% to 25% of taxable income. Special rules apply to business entities other than C corporations.

The IRS urges all taxpayers to keep records supporting their charitable deductions. Most gifts require obtaining an acknowledgment letter from the nonprofit. Gifts of property may require filing an additional IRS Form 8283. Gifts of property valued in excess of $5,000 may also require a qualified appraisal.

Editor's Note: Some donors with large IRAs are taking substantial distributions this year and making major gifts to their favorite nonprofits using the 100% AGI limit. Others who have large incomes or have sold a highly-valued property may also choose to give generously under the 2021 expanded gift rules.